Show me the money! Why is Crezco free?

Wednesday, 19 October 2022, 3 minute read

It wasn’t easy ‘selling’ Crezco to the SME community as a solution for collecting invoicing payments. Businesses have had decades to familiarise themselves with card payments and brands like PayPal and Stripe, whereas nobody had heard of ‘Crezco’ or ‘account-to-account’ payments. Any payments company needs to be deemed trustworthy by its target audience, but when we told them our payments were free they knew it was a scam! We were in the same bucket with the Nigerian prince and his Swiss vault full of cheese. The less skeptic prospects had two other equally adamant theories behind our free solution for collecting payments from customers. Either we were: a) hiding the fees somewhere nasty and not being honest with our customers; or b) Crezco was being run by financially incompetent individuals. The latter point could be true, but we had two good reasons for making our account-to-account payments free: ‘Gross Margins’ and ‘Product Lead Growth’.

Gross Margins

Gross margins are net sales after cost of goods sold (COGS). If a pint of milk at Tesco’s cost 90p, but Tesco paid the cow 50p for the pint, Tesco’s gross margins are 40p (44%) per pint. The lowest price Tesco could pay without incurring a loss (ignore refrigeration, transportation, packaging and storage costs) would be 50p. Free milk would be heavy loss leader and would be a very bad idea (unless it increased the sales of biscuits too).

Milk isn’t the same as payments, but payment technology giants like PayPal also have COGS. PayPal acquires the customer, PayPal own the customer relationship and customer contract. PayPal also decides how much the customer is charged and if something goes wrong the customer blames PayPal.

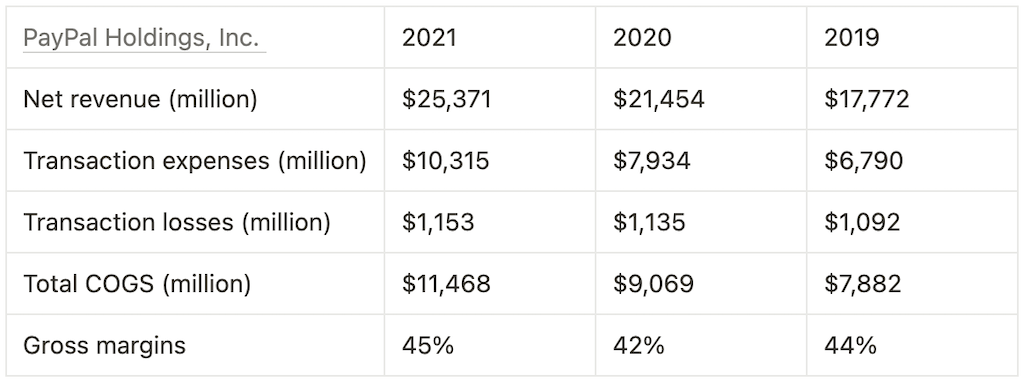

However PayPal is not the only company involved in the payment transaction and these other companies need to get paid, just like the cow. PayPal calls these costs ‘transaction expenses’: fees paid to payment processors and other financial institutions when we draw funds from a customer’s credit or debit card, bank account, or other funding source they have stored in their digital wallet.’ These transaction expenses accounted for 41% of PayPal’s revenues last year (see Table 1). Perhaps it isn’t surprising Visa and Mastercard reported $24.1bn and $18.9bn in revenue, respectively.

As seen in Table 1, not only did PayPal have to collect a minimum of £10.3bn in revenue just to cover its own transaction expenses in 2021, PayPal also needs to cover their ‘transaction losses’: the expenses associated with buyer and seller protection programs, fraud, and chargebacks. Seller protection is where PayPal agrees to cover you (the merchant) from chargebacks, so long as you’ve provided sufficient documentation of product delivery and arrival within 7 days of being notified. Basically, its insurance and like all insurance company they’re better at collecting than distributing.

Crezco is different to both PayPal and Tesco. Our domestic account-to-account payments have no COGS. Account-to-account payments disintermediate the card collection ecosystem (payment service providers, payment schemes, merchant acquirers, card issuers, etc.). For domestic account-to-account transactions, whether GBP to GBP or EUR to EUR, there is no cow to pay. For this reason our domestic payments are free.

*We do occasionally initiate domestic payments via third-parties such as Yapily, TrueLayer and Token, and for this we are charged a fee, which is COGS but it’s our gift to you.

Having repeatedly highlighted the term domestic, it is no surprise that our international payments do have COGS. For this reason, and others, we charge a small transaction fee for handling cross-border payments. For the purpose of honesty and transparency, I’ll give you an example of some of the COGS. In order to convert currency X (funding currency) to currency Y (payout currency) we need to have a ‘bank account’ which accepts the currency X. These ‘bank accounts’ charge a fixed fee per payment we receive, which differs depending on the currency. Remember we handle 70+ currencies.

As an example, it cost us £0.20 to receive any GBP payment and €0.25 to receive any EUR payment, but more esoteric currencies cost more. Once we’ve received the funding amount in currency X we can swap it, via our institutional brokers (who trade billions daily but still charge us a small fee), for currency Y (the payout currency). However now we have currency Y (the payout currency) we have to move the funds to a bank account in country Y and initiate a payment on currency’s Y local payment rails. Again, for this we are also charged a fee. For example, if the currency is USD we have to initiate a FedACH payment which costs us £0.30. If the currency is AUD we initiate a payment via AusPayNet which costs £0.40 and were the currency NOK we would initiate a payment on the Norwegian Interbank Clearing System for £0.40. Each local payment rail has a different cost. These are our COGS on international business payments.

What are the cost of our cross-currency transfers?

Product Lead Growth

Companies don’t just generate revenue (charge fees) to cover their COGS. There are also operating costs to pay for, which include salaries, rent, R&D and marketing expenses. Even if there are no COGS involved, we still need to pay our operating costs. Crezco isn’t a charity and neither are those that work here.

However, having generated investment by selling shares in Crezco to venture capitalist investors, we have accepted that we will temporarily operate at a loss. This is because we are focused on product lead growth.

What is product lead growth? The MBA handbook describes it as a strategy which prioritises production adoption, customer stickiness and advocacy. If you work at Crezco, you would have heard me say the most valuable asset on a company’s balance sheet is happy customers. It may sound obvious, but this is not a self-evident strategy adopted by all companies. A sales-led or marketing-led organisation will have very different priorities.

Here are a few key pillars and characteristics of product lead companies:

Build for the user, not the buyer

Stripe (grrr… cards 👿) was famously ‘built by developers for developers’. When designing Crezco, I always imagined a Worldpay sales executive entertaining a CEO on the golf course. The CEO returns triumphantly to the office to announce he has negotiated excellent rates for all Worldpay transactions. The CTO shrugs his shoulders and states they’re using Stripe regardless, sorry. The boss is no longer the decision maker, the user is. It was the same with other superstar companies like Airtable, Dropbox, Zoom, Slack, Calendly, and others. Customer Centric is one of Crezco’s five company values, but maybe we should update it to User Centric.

Deliver value, then capture it

Users are clever and don’t trust strangers. They now have limitless online options. Instead of selling to user by listing how great all your products and features are, just let them use it and discover the truth on their own. The ubiquitous nature of technological developments like the internet (though really the world-wide-web, because before the www the internet sucked) haven’t just changed what we buy, but also how we buy. Sales and marketing worked during the Age of Ignorance, but customers (users) are clever and will not be tricked into buying a bad product and if they do, they’ll drop it as quickly as they picked it up. First you gain their trust, then you start introducing them to more ‘premium’ products. The “paywall” comes last, not first, and pricing scales alongside extracted customer value. Just think of those companies like Airtable, Dropbox, etc.

Not all customers generate cash

It’s quite common that 80% of a company’s revenue derive from 20% of their customers. It is less common when 80% of your customers don’t generate a dollar between them. However, this is true for companies like Zoom, Dropbox and Slack. These publicly listed companies (Slack was) highlight that it is only a fraction of their users who generate revenue. Some customers like to tell us they will never use our premium products of features. That’s fine and we’re still happy to have them. Why? As a pure software company, we can acquire these users at zero marginal cost. Furthermore, if they don’t generate Crezco revenue, they can still become Crezco product advocates (help with referrals) and provide us great feedback data for our product backlog so maybe one day we will have what they want enough to pay for.

Offering free domestic payments isn’t a scam and neither do we think we’re being financially irresponsible. Rightly or wrongly, offering free domestic payments was a planned strategy. We do generate revenue, on international business payments and by placing some features and products behind a paywall, such as our accounts payable solution and our branded business checkout. Hopefully you find them of sufficient value to pay for, but if not, no worries, you’re welcome to continue using our free domestic payments for as long as you like.

About the author: Ralph Rogge - CEO at Crezco

With a background in both technology and payments, Ralph saw the introduction of open banking payments as the missing technological innovation required to better address invoice payments. At Crezco, Ralph focuses on building a strong culture and awesome products. Ralph believes a product should be so intuitive you could use it with your eyes closed.